Digital Asset Treasury (DAT) companies have become one of the most intriguing capital markets phenomena of the current crypto cycle. From Wall Street to Tokyo, investors are increasingly drawn to publicly listed companies whose primary value proposition is the accumulation and optimization of digital assets—primarily Bitcoin and Ethereum, slowly spilling over to other long tail assets. These firms offer equity-like exposure to crypto assets without the frictions of self-custody, tax complexity, or regulatory constraints often faced by direct holders.

But are DATs a sustainable investment category, or are they merely a high-beta wrapper riding the current bull cycle? This article introduces the DAT concept, explores the upside and risk factors, outlines how the space is evolving, and ultimately tackles the central investor question: Is this a durable new asset class or a temporary arbitrage opportunity?

A DAT company is a publicly traded entity that accumulates digital assets—most commonly BTC, ETH, or SOL—as a core balance sheet strategy. These companies do not rely on traditional business models (e.g., SaaS revenue or manufacturing), but rather seek to deliver crypto exposure to investors through a regulated, equity-based instrument.

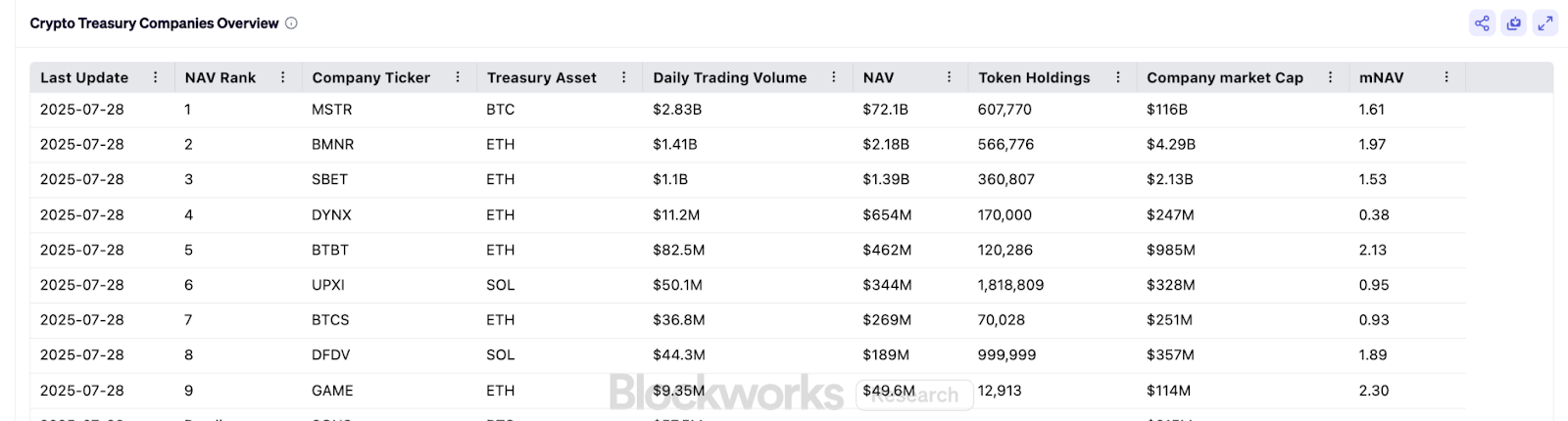

The modern DAT movement was pioneered by MicroStrategy (MSTR), which began acquiring BTC in 2020. Its strategy was simple yet radical: use equity, and low-cost debt to accumulate as much Bitcoin as possible. Since then, new entrants like Metaplanet (3350.T) in Japan and Semler Scientific (SMLR) in the U.S. have followed suit, some transforming from sleepy businesses into full-fledged crypto treasuries. The type of underlying digital asset in this type of play has also expanded into ETH (Example, SBET and BMNR) , Sol (Example, UPXI, DFDV) and many other long tail assets.

As Keyrock explains in their “BTC Treasuries Uncovered” report, these companies serve as a “gateway” for traditional capital markets to access crypto, often with structural advantages in tax, liquidity, and regulatory compliance.

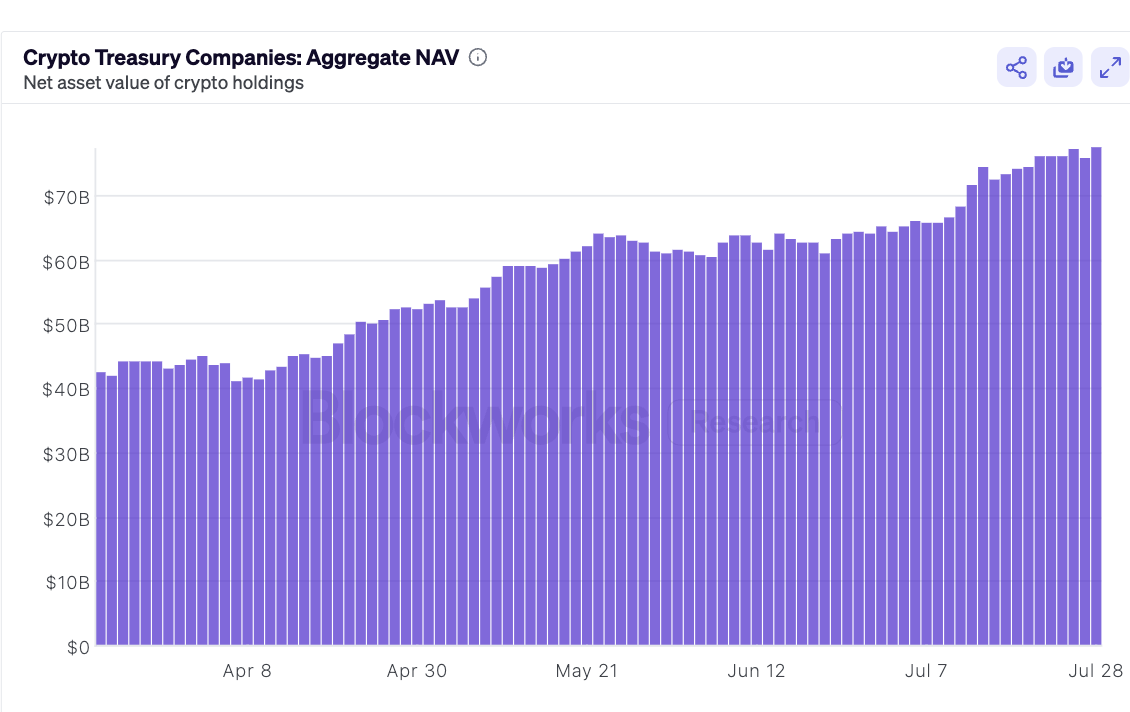

As of now, DATs have accumulated more than $70B worth of Digital assets.

Many institutions—such as pension funds, family offices, and insurance firms—face regulatory, operational, or tax hurdles when investing in digital assets directly. DATs solve this by offering a listed equity that acts as a proxy for crypto exposure. This opens the market to a broader investor base, especially those constrained by mandates that prohibit direct digital asset holdings or those seeking exposure in retirement accounts (e.g., IRAs).

Moreover, in certain jurisdictions, investors may face less onerous tax treatment when buying equities (e.g., capital gains on stocks vs. income tax on crypto trades). DATs can also provide better audit trails and custody standards, reducing the perceived risk for regulated entities.

DATs can structure their capitalization to attract various types of capital. Some offer:

This segmentation allows investors to choose a risk/return profile that matches their appetite—unlike spot BTC/ETH or ETF which has no capital structure hierarchy or BTC mining stocks which introduce different sets of operational risks.It also allows the company to diversify its funding sources over time, supporting sustained accumulation.

DATs like MicroStrategy have pioneered a model where they raise fiat capital through equity or low-interest debt, then convert it into BTC. If their shares trade at a premium to NAV, they can issue more shares and reinvest the proceeds at a multiple of intrinsic book value. This reflexive loop allows for compounded crypto accumulation, measured by a key metric called BTC yield -A positive BTC Yield indicates that the company is increasing the amount of BTC each share represents.

Moreover, many DATs are beginning to pursue productive strategies for their treasuries—such as staking ETH, participating in validator networks, or lending BTC at yield. This transforms a passive treasury into a potential yield-generating asset.

I have seen investors argue that DAT companies offer asymmetric risk/reward, particularly relative to owning the underlying token, in a “heads you win, tails you don’t lose much” situation. Upside – “heads you win”: the near-term upside is the potential NAV premium and the longer-term upside comes from growing NAV-per-share and sustaining that premium. Downside – “tails you don’t lose much”: downside is limited because even if the company does not trade at a premium, investors invest at roughly 1.0x NAV and still retain their pro rata share of the underlying NAV and the underlying token return (e.g., spot BTC, ETH).

I would argue that downside is probably more than what investors are willing to stomach in light of below risk factors.

While simpler in business model than traditional firms, DATs face crypto-native operational risks:

A misstep—whether through theft, governance failure, or loss of access—can damage credibility and destroy shareholder value.

DATs operate like externally capitalized asset managers, relying on continual fundraising and asset allocation discipline. Key risks include:

If market cap falls below the company’s crypto holdings (i.e., trades below 1.0x mNAV), and they are unable to reverse this trend, investor outflows or a funding freeze can trigger a reflexive death spiral.

DATs are sensitive to intertwined market risk factors:

Particularly, for retail investors who do not necessarily have the opportunity to get into those deals at 1x NAV through PIPE deals or other sophisticated instruments that are largely only available to institutional investors. They need to be cognizant of the right “entry point”.

Consider the case of SBET (SharpLink Gaming) as a cautionary example of the volatility and complexity involved in DAT investing. Following the announcement of a $450 million private placement on June 2, the stock surged to $79, only to plummet to ~$9 shortly after the registration of new shares on June 12. It subsequently rebounded to $40 due to ETH appreciation and aggressive accumulation of ETH within a short period of time, before settling around $19—all within a span of two months.

What many retail investors often overlook is the effective cost basis of the newly issued shares from these PIPE (Private Investment in Public Equity) deals. In SBET’s case, the PIPE investors entered at $6.15 per share, meaning that even at current levels—well below the perceived 1.0x mNAV—they are still sitting on significant gains. This creates selling pressure that is not necessarily tied to NAV but instead to earlier, favorable entry prices.

Moreover, accurately tracking a DAT’s mNAV in real time is nontrivial. Several dynamic factors affect it:

These variables introduce opacity into the true economic exposure of new investors. Unlike a clean ETF structure, retail participants often have limited visibility into whether they are buying at a premium or discount to the actual, fully diluted mNAV.

In SBET’s case, even if the current 1.0x mNAV implies a price of $13 per share, PIPE investors—already up over 2x—may still sell below NAV simply to lock in profits. This decoupling between market price, NAV, and cost basis illustrates one of the structural complexities that DAT investors must understand to avoid being on the wrong side of the trade.

Regulatory clarity and capital market dynamics play a big role. Japan’s cheap debt financing and hunger for yield allowed Metaplanet to quickly attract retail and institutional capital. Similarly, U.S.-based firms benefit from deep capital pools and retail trading access via platforms like Robinhood or IBKR.

Companies with strong investor relations and a clear treasury growth narrative can raise equity at accretive multiples to NAV. This not only enhances BTC/ETH per share metrics but also builds investor confidence. The ability to issue shares above NAV is a flywheel for treasury growth.

Every DAT needs a “ Michael Saylor” or “Tom Lee”.

DATs succeed when their leadership understands:

Teams with both traditional finance and crypto backgrounds (e.g., MicroStrategy, BNMR) are especially well-positioned.

Beyond accumulation, the future of DATs will include:

This productivity will drive yield generation, help differentiate business models, and improve capital efficiency—while also tying the DAT more deeply into the ecosystem it supports.

DATs represent probably more than just a bull market narrative. They reflect the convergence of two powerful forces: Crypto as a monetary revolution and Public equities as a capital formation machine.

The most successful DATs will not only offer crypto exposure, but also become ecosystem contributors—validators, DAO voters, and infrastructure financiers.

“DATs could evolve into the Grayscale 2.0—only more capital efficient and more crypto-native.” – Keyrock

However, mismanagement or leverage abuse could turn them into zombie wrappers, trading at deep discounts, unable to raise capital or execute. Even worse, if they are used as a vessel to accumulate the types of digital assets that might be worthless in the long run, no matter how many wrappers you put on top, the vessel will eventually destroy investor value and leave investors burnt.

For investors, the key is discernment: differentiate between opportunistic wrappers and long-term builders. The former will fade with market cycles. The latter could become the BlackRocks of crypto.

Disclaimer: Content above may feature projects that LongHash is invested in. It is not an investment advice and does not constitute any offer or solicitation to offer or recommendation of any investment product.

References: